Why your pension savings can go up and down

Market volatility is a normal part of long-term investing

Watch our short video where James Lawrence, Chief Investment Officer at Smart Pension, explains what market volatility means for your pension and why staying focused on the long term matters.

How are my pension savings invested?

Your pension savings are invested in the world around us. The main ways of investing are owning part of a company (equities or shares), lending to companies (bonds) or lending to governments (gilts or government bonds).

You access these investments through “funds” which pool together money from lots of people to invest as one. Your money in the fund is shown by the number of “units” you have bought with your pension savings. These units have a price which can go up or down, which is the return you see in your investments.

You can make changes to your investment funds at any time through your Smart Pension member account or the Smart Pension app. If you do not make a choice, your savings are automatically invested in an investment strategy which invests in chosen funds on your behalf. The default investment strategy targets an allocation at retirement which is suitable to take a flexible income in retirement. There are two other retirement targets which can be chosen: an annuity purchase and cash.

Sign in to your account to learn more about the investment options open to you.

Why are my investments going up and down?

You can make changes to your investment funds at any time through your Smart Pension member account or the Smart Pension app. If you do not make a choice, your savings are automatically invested in an investment strategy which invests in chosen funds on your behalf. The default investment strategy targets an allocation at retirement which is suitable to take a flexible income in retirement. There are two other retirement targets which can be chosen: an annuity purchase and cash.

While we can’t control the impact of these changes on investments, we look to offer a range of investment options. For the default investment strategy, we look to reduce the fluctuations by using lots of different types of investments, which are suitable for the long term. Your pension savings are invested for your future retirement and the aim is to provide strong outcomes over the long term.

All investments involve some degree of risk and you should think about your risk tolerance when you’re choosing your investments for your pension savings. Our default investment option has a long-term outlook and, although investments may go up and down in the shorter term, over the longer term they are expected to produce a positive return.

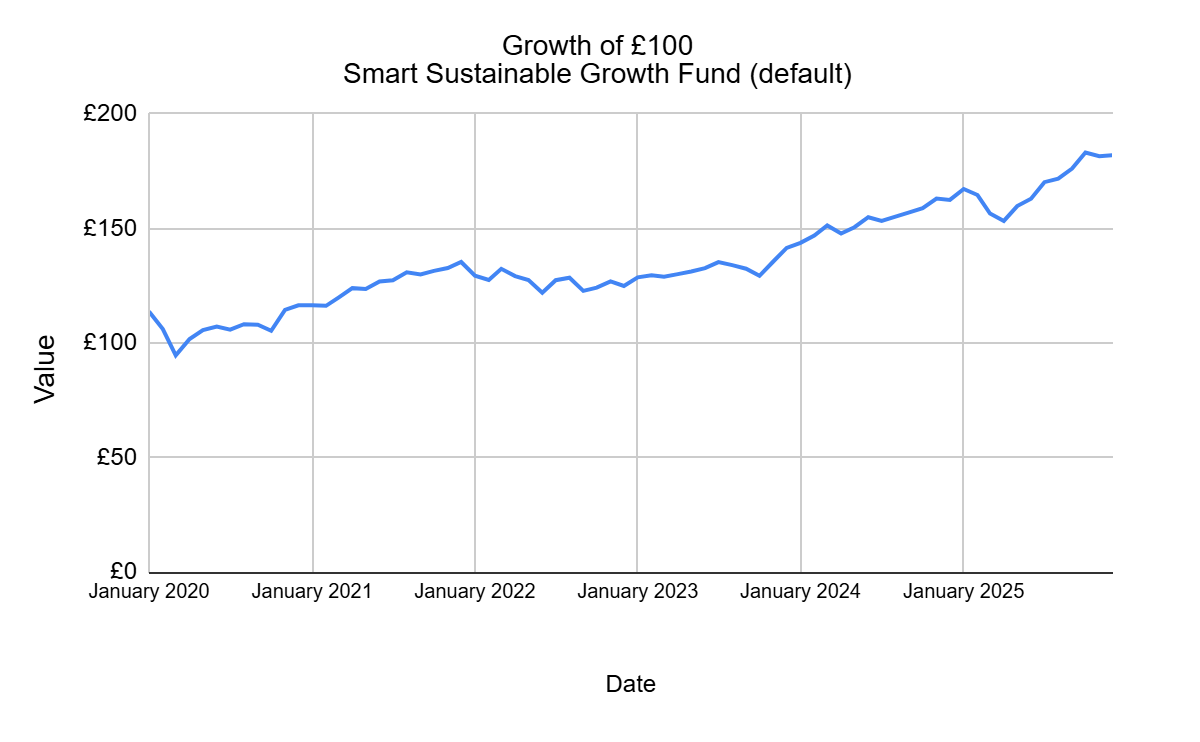

The chart shows the investment return of the Smart Sustainable Growth Fund, used in our default investment strategy, from January 2020 to December 2025. As you can see, the value of the £100 has gone up and down during this period, but over the entire period, the value has increased. Notably, there was a big fall in returns at the start of 2020, as a result of the global pandemic. This had recovered by the end of the year.

Gross performance, monthly data

Source: Mobius Life

Why may I see a bigger fall than usual in my investments?

Investments can go up and down in the shorter term. Over the longer term they are expected to produce a positive return, meaning that you have more money at retirement than you saved, which will help provide a good retirement.

Recent events in the Middle East, including military action involving the U.S., Israel and Iran, have led to short-term market volatility, with share prices moving up and down more sharply and energy prices rising as investors react to uncertainty. While these movements can feel unsettling, it’s important to remember that pensions are designed as long-term investments. Over time, markets have consistently weathered geopolitical crises, conflicts and economic shocks, and long-term investors have historically been rewarded for staying invested. Pension investment strategies are built with diversification and long-term horizons in mind to help manage periods of uncertainty and support members’ retirement goals.

If you are close to retirement, you may wish to take this opportunity to review your retirement target and the funds you have chosen, as well as your selected retirement date. Ensuring these remain aligned with your plans and risk comfort.

History shows that even after periods of significant geopolitical tension and market disruption, markets have recovered over time. In August 2024, fears of a US recession triggered volatility across global markets. The Japanese Nikkei 225 index suffered its worst day since October 1987 (the Black Monday crash) and the sell-off continued in Europe. In 2022, global investments were negatively impacted by Russia’s war in Ukraine, rising inflation and the cost of living and UK policy shocks.

Investment downturns have occurred multiple times before and are likely to happen again in the future – they are a normal part of investing. Whilst we can’t predict the future, past events show us that investment downturns have been followed by periods of recovery and growth.

On Monday 19th October 1987, also known as Black Monday, global investments fell more than 20% in a single day. It is widely thought that slow economic growth, investor panic and relatively new computer-driven trading models drove the downward spiral. Black Monday had knock-on effects on global economies, but with the help of central banks these economies fully recovered within a couple of years.

During the Global Financial Crisis of 2008-2009, Financial Times market data reported that the FTSE 100 (UK stocks) fell by over 31% in 2008. Governments intervened, central banks cut interest rates and more regulations were introduced to provide safety nets for investors. Investments bounced back quickly, with the FTSE 100 recovering c. 22% the following year.

While we do not have a crystal ball to tell the future and cannot guarantee investments will always bounce back, we can see how investment cycles have behaved in the past. Some investments may do poorly compared to other investments over short time periods, and the opposite might happen in other time periods. Therefore, our default investment option diversifies across different investments, as well as increasing its allocation to investments known to be less risky as a member approaches retirement. We monitor investment performance on a regular basis with our appointment of external advisers.

What should I do when my investments fall?

You can make changes to your investments whenever you like. However, please be aware that “panic selling” can crystallise losses and potentially harm your future returns by missing out on the positive days. In times of high volatility, it is important not to panic or make any rash decisions about changes to your investments, including transfers and claims.

Our investment strategies look to provide strong returns by investing over the longer term across diversified investments rather than trying to profit from short-term turning points. You may wish to check that your investment choices reflect your longer-term goals, as some individual funds and asset classes have different levels of risk and potential returns.

If you are close to retirement and in a predetermined investment strategy, you may wish to review the retirement target you have chosen and your retirement date. If you would like personalised advice, you should get in touch with an independent financial adviser. If you do not have an independent financial adviser, you can find information through the MoneyHelper website.

Contributions to your pension savings are taken and invested monthly, unless you choose otherwise. These regular contributions can smooth out the ups and downs of investment returns. If investments are doing well, they will be more expensive to buy. If investments aren’t doing well, they will be cheaper to buy. Purchasing investment units every month therefore means the cost should even out over time, and you’re investing in both good and bad market environments.

Where can I find my investments?

You can find your investment options by signing in to your Smart Pension account and clicking the ‘Investments’ tile on your dashboard. Get help signing in here.

If you want to read more about our investment approach, read our latest guide here.