Can a salary sacrifice pension help with the National Insurance increases?

Smart Pension’s Claire Misata shares her view

In her Autumn Budget, the Chancellor Rachel Reeves announced that an increase in employer’s National Insurance Contributions (NICs) would be introduced in 2025. This change means there’s been an increase in the awareness of salary sacrifice pension schemes, which offer savings and a tax-efficient pension boost for employees. If you haven’t yet explored salary sacrifice, now may be the perfect time – a win-win for you and your team.

What is salary sacrifice?

Salary sacrifice, also known as ‘salary exchange’, is an arrangement with you and your employees, under which an employee agrees to exchange part of their salary equal to the amount they want to contribute to their pension. You will then pay this amount, plus your contribution, direct to their pension savings.

How can salary sacrifice benefit my company?

Salary sacrifice brings savings and benefits for both your business and your employees through tax efficiency. Both you and your employees pay less in NICs each month, at no extra cost to you. You can choose how to reinvest those savings – some employers choose to use the savings to offer an increased pension contribution to their employees.

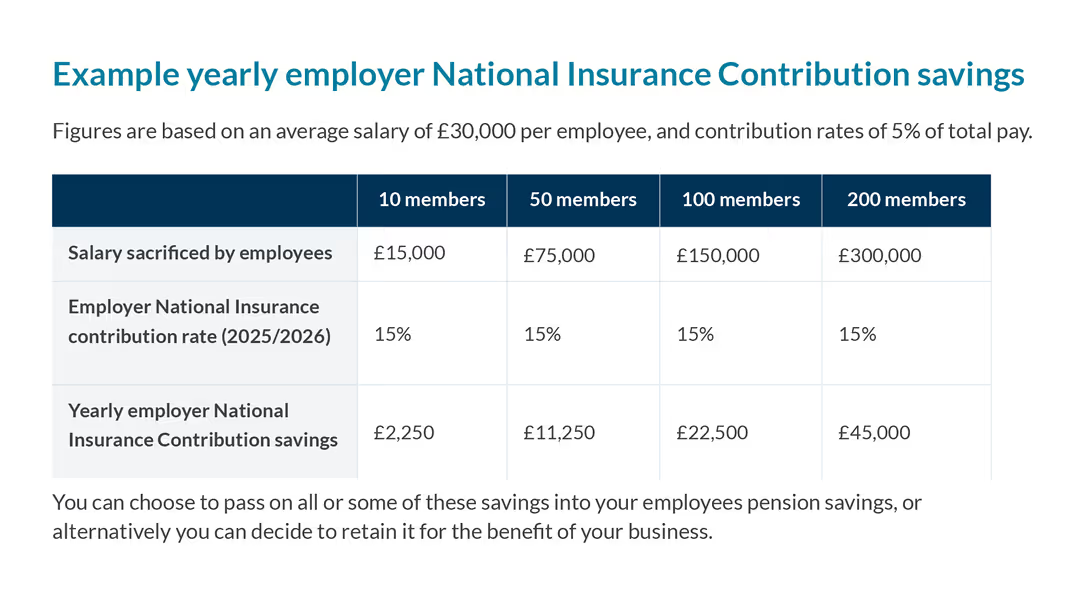

At Smart Pension, we’ve helped businesses like yours achieve meaningful savings with this straightforward approach. While not all pension providers offer it, we believe salary sacrifice is one of the most effective ways to cut costs and boost employee benefits at the same time. For instance, an employer with 50 employees, each earning around £30,000 and contributing 5% of their salary to their pension, could save more than £10,000 a year.

If you employ more than 50 people, the potential savings are even higher, as detailed below.

Find out more about these savings in our short guide to salary sacrifice.

How salary sacrifice can benefit your employees

The benefits of salary sacrifice aren’t just for you as the employer, but they also benefit your employees. Let’s look at a worked example to show how it can make a real difference to one of your employees.

Jason earns £30,000 a year and sacrifices 5% of his salary to his pension, which equates to £1,500 a year. If Jason’s employer paid the NIC savings into his pension, he would see little or no difference in his take-home salary, while seeing an extra £120 a year paid into his pension.

The real benefits come when you look over a longer period. Jason would see a considerable difference in his pension savings when he looks over the longer term, as detailed in our member guide to salary sacrifice.

- £1,774 more in his pension pot after 10 years

- £5,263 more in his pension pot over 20 years

Interested in finding out more?

Interested in learning more about how salary sacrifice can benefit your business and employees before the changes in 2025? Read more about why an employer should choose salary sacrifice.

Book a call to talk to one of my team today or email us at [email protected]

Tel: 0330 124 7409

Disclaimer

All figures given are estimates only, any savings are not guaranteed and any amounts will vary based on particular circumstances. Smart Pension can only provide guidance and is not regulated to give financial advice. If you require professional advice, you can find support on the MoneyHelper website.

About Smart Pension

Launched in 2015, Smart Pension now exceeds £10bn in Assets Under Management (AUM) and serves 2 million members and 100,000 employers. It is powered by Keystone, Smart’s global savings and investments technology platform.

Aquiline, Barclays, Chrysalis Investments, DWS Group, Fidelity InternationalStrategic Ventures, J.P. Morgan, Legal & General Investment Management, MUFG and Natixis Investment Managers are all investors in Smart Pension.